Family investment companies

Learn what a family investment company is and how they work

If you're looking to pass on your wealth in a tax-efficient way, a family investment company could be a good solution for you. Talk to our expert solicitors to learn how a family investment company could help you.

Contact usWhat is a family investment company?

A family investment company is a private limited company based in the UK, where all shareholders are family members and which invests rather than trades.

Family investment companies are becoming increasingly popular as a way to secure family wealth, being straightforward to set up and a flexible and very tax-efficient way to invest cash to generate income for the family, keep control of assets and pass them to the next generation — particularly if you're familiar with how a business operates. They are being used as an alternative to trusts for Inheritance Tax planning when an individual, typically, has cash assets of £1m plus.

A further attractive benefit is that family investment companies are taxed according to corporation tax rates, which are significantly lower than personal income tax rates.

If you'd like to consider a family investment company as part of your strategy for inheritance, succession and wealth planning to meet your family’s unique requirements, our expert solicitors can guide you through the legal process and help to ensure that your family investment company is fit for purpose.

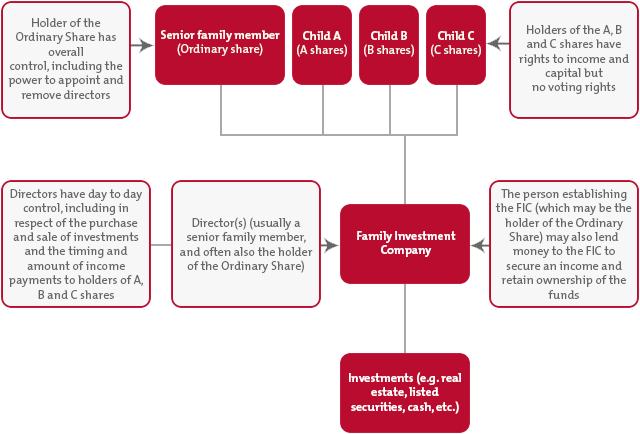

Structure of a family investment company

There is a great deal of flexibility as to how the family investment company can be structured but typically each family member who is to benefit from the family investment company will hold a different class of share. These shares give the family members the ability to receive such income (in the form of dividends) as the directors declare. The shares also provide an entitlement to capital (in defined amounts or proportions) in the event of a sale, return of capital or the winding up of the family investment company.

The founder of the family investment company will usually also hold shares. The founder’s shares would not normally carry any rights to receive significant value from the company (although if this is desired, to some extent, value can be retained by the founder), but do carry voting rights, giving the founder control over the appointment of directors. Where the founder is a director, he has control over how the company is run including the investment of assets and declaration of dividends.

The founder shares will pass on death in accordance with their Will which can provide a further layer of management and protection for family wealth.

Benefits of a family investment company

Asset protection

- The articles of association of the family investment company can include provisions to prevent any share transfers to members' spouses. In divorce proceedings, the courts are very reluctant to order a transfer of shares that is not permitted by the company's articles. This protection can be further enhanced by the family members holding their shares via nominees.

Retaining control

- The founder controls the appointment of the company's directors. The company's directors retain control over the investments within the family investment company. The directors can also decide which of the family shareholders receive dividends. Alternatively, the directors may choose not to declare any dividends and allow funds to roll up and grow within the company or reinvest them. No shareholder has a right to receive either income or capital from the family investment company.

Taxation

- No lifetime inheritance tax charges arise on transferring sums to the family investment company irrespective of the value transferred. This makes them very attractive compared to trusts which have a 20% entry charge for amounts transferred above the nil rate band (£325,000).

- Sums held within the family investment company are outside of the founder's estate for inheritance tax purposes. Provided the founder survives for seven years from creating the family investment company, amounts held within it will escape inheritance tax on the founder's death.

- Unlike trusts, family investment companies do not face an inheritance tax charge every ten years. The value of the shares held by a family member would be taxable in the event of his/her death, although the value of the shares will generally be lower than the value of the underlying investments.

- The current rates of corporation tax at which any income and capital gains are taxed within the family investment company are significantly lower than the top rates of income tax and capital gains tax payable when assets are held in trust or held directly by family members. In particular where the family investment company holds shares dividends paid on these are not taxed within the Family Investment Company. If the profits are to be retained within the company no further tax would be payable but there will be further potential tax charges on any distribution of income or capital to the shareholders. There is therefore an element of double taxation which can reduce the overall tax benefits, but there remains a far greater degree of control over the incidence and timing of tax charges upon the individual family members.

Privacy

- If the company is set up as a limited company, it is necessary to file annual accounts with Companies House. To maintain confidentiality, the family investment company can be set up as an unlimited company for which there would be no requirement to submit annual accounts.

Get in touch

Ready for the next step? Talk to our experts in family investment companies.

Contact usOur other private wealth services