Learn what a section 431 election is, when you may need to make one and the benefits and risks in this comprehensive guide.

It is common where shares are being transferred or issued to employees or directors, for the individuals concerned to be asked (or even required) to complete a section 431 election. But what is a section 431 election and why do you need to make one? Tax expert, Haydn Rogan, explains.

What is a section 431 election and why do I need to make one?

Employees and directors (whether executive or non-executive) who subscribe for or acquire shares in the company or any member of the group for which they work are within the scope of special tax rules applying to employment-related securities.

It should be noted that the rules apply to all officeholders including non-executive directors even though they are not technically employees and cannot be sidestepped by issuing the shares to family members or other connected persons.

The rules apply to UK resident employees and directors who work for and acquire shares in overseas companies but do not generally apply to non-UK resident employees or directors who do not carry out any duties in the UK (and are therefore not subject to UK PAYE and NICs).

The rules can also apply to former or prospective employments so, for example, will apply to investors who are to be appointed directors.

The essence of the rules is to prevent employment income or reward from being passed to employees or directors (or any persons associated with them) by way of capital returns in relation to shares or securities.

One of the ways this was achieved in the past was by giving employees or directors restricted shares whose market value, at the time they were issued, was suppressed by virtue of the restrictions attached to them.

The restrictions would then either fall away or be removed, leaving the employee with a much more valuable asset.

How section 431 elections work

A section 431 election changes the timing (and potential amount) of income tax that is payable in relation to restricted securities.

For tax purposes employment-related securities have two values:

- Actual market value (AMV) i.e. what the shares are actually worth; and

- Unrestricted market value (UMV) i.e. what the shares would be worth if there were no relevant restrictions attaching to them (for example, on the ability to sell or transfer them) whether those restrictions are set out in the articles, investment agreement, shareholders’ agreements or elsewhere.

In very broad terms, unless the ‘employee’ pays the full UMV for the shares as at the time of their acquisition (or elects, for tax purposes, to be treated as having acquired the shares at their UMV as set out below), part of the future growth in value of the shares may fall to be taxed as income rather than capital.

There is always an immediate ‘general earnings’ tax charge to the extent that the director/employee does not pay AMV for the shares at the point of acquisition.

If the shares are readily convertible assets (which essentially means if they can be easily exchanged for cash) then such income tax will have to be accounted for and collected by the employing company via PAYE and NICs (both primary and secondary) will also be due on the notional payment (i.e. the discount to AMV).

If the shares are not readily convertible assets then income tax will need to be reported and paid via the individual’s personal tax return for that tax year rather than by the company through payroll and no NICs will be payable.

The director/employee can, however, elect by way of a joint section 431 election with the employing company, to also be taxed also at the point of acquisition on any discount between the UMV and AMV.

The purpose of a section 431 election is to effectively ignore all/some of the restrictions in valuing the shares at acquisition/subscription and treat the shares as having been acquired at their UMV. The definition of restriction is wide and most private company articles contain ‘restrictions’.

If the director/employee does not pay full UMV for any shares that are transferred or issued to them by reason of their employment then, on a subsequent sale, HMRC can seek to levy an income tax charge under the restricted security provisions on a proportion of the growth in value of the shares.

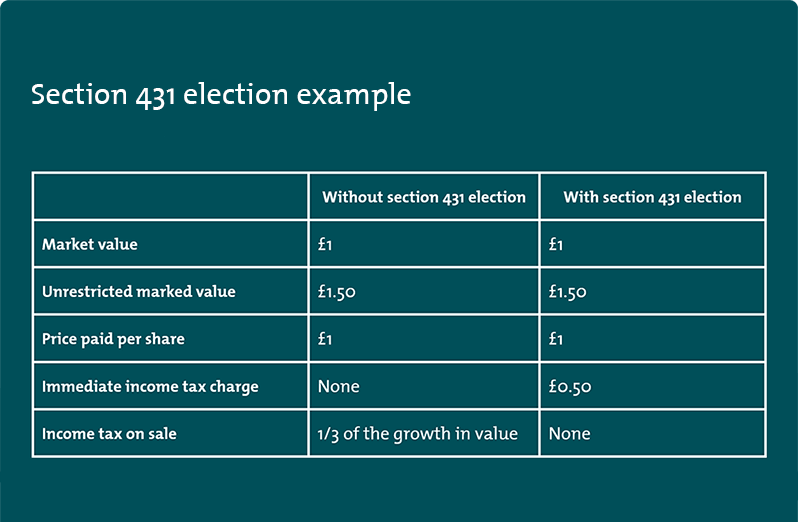

To illustrate, if at the point of acquisition by an employee the actual market value of a share is £1 and the unrestricted market value is £1.50 and the employee pays £1 per share there would be no immediate income tax charge (as the employee has paid the AMV) but on a subsequent disposal of those shares, 1/3 of the ‘gain’ (the growth in value over £1) could be subject to income tax (as only 2/3 of the UMV was paid up or subject to tax on acquisition).

If, however, a s431 election is entered into, whilst there would be an immediate income tax charge on the £0.50p discount to UMV (£1.50 less the £1 paid) any subsequent growth in value would not be subject to income tax under the restricted security provisions.

Benefits and risks of a section 431 election

The broad purpose of the election is, therefore, to treat the shares as having been acquired at their unrestricted market value and try and ensure that any future growth in value of the shares is taxed as capital, not income.

It should be noted that there could be a potential downside in making the election if the shares were to fall in value. However, if you expect the shares are expected to rise in value then an election is generally desirable (and from the employing company’s perspective protects against future potential employers’ NIC charges).

When to make a section 431 election

A section 431 election must be made within 14 days of the acquisition of the shares. Employers often ask employees to agree to the election as part of the share grant process, as it may be too late to do so later.

The election can be made through various means, such as email or as part of the share grant process.

Section 431 elections do not need to be filed with HMRC but a copy should be kept by both the individual and employer in case of any subsequent tax enquiry (where HMRC may request a copy of the election).

HMRC will also be notified as to whether or not a section 431 election was entered into via annual online employment-related securities returns that are required to be submitted by the employer.

Can we help?

If you have any questions regarding section 431 elections or need advice on any tax issues surrounding employment-related securities or the acquisition, sale or transfer of shares generally, please contact Haydn Rogan, a partner in the Corporate department on 0161 214 0517 or by email to haydn.rogan@weightmans.com.

A version of this article was first published on 6 Jun 2015